When you’re in the market for a home, it’s essential to understand the difference between conditional vs pre-approval. Both terms relate to a lender’s assessment of your ability to secure a mortgage, but they are not interchangeable. Conditional approval means the lender has agreed to loan you the money, contingent on meeting specific conditions before final approval. Pre-approval, however, is an initial assessment based on your financial details, indicating that you’re likely to be approved, but it doesn’t guarantee a loan.

In this article, we’ll explore the key differences between the two and help you determine which option is best suited for your home-buying journey.

Table of Contents

ToggleWhat Is Pre-Approval?

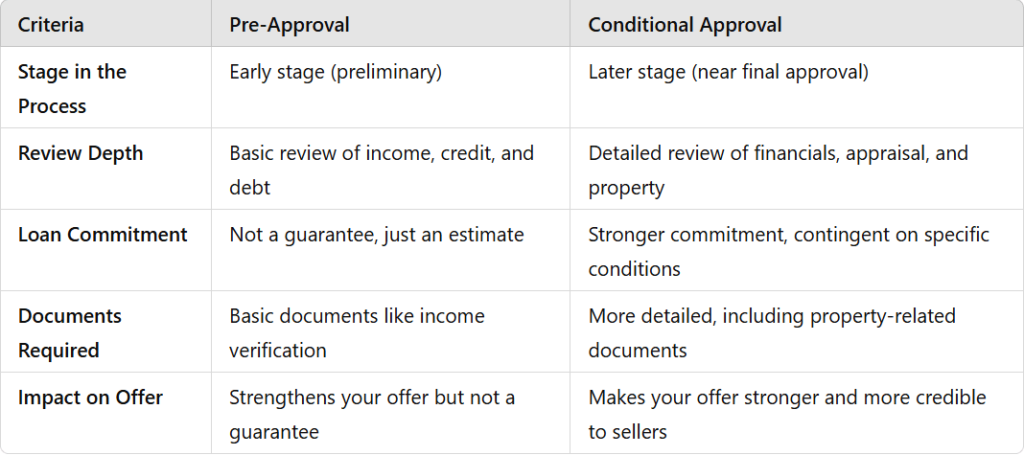

Pre-approval is often the first step in the home-buying or investment process. It involves the lender reviewing your financial information to estimate how much they are willing to lend you. The pre-approval process is typically quicker than full approval and gives you a clearer picture of your budget.

Pre-Approval Process:

-

- Documents Needed: Income verification, employment status, debt-to-income ratio, and credit score.

-

- Outcome: A letter indicating how much you can borrow, usually valid for 60-90 days.

-

- Reliability: While pre-approval carries weight, it isn’t a guarantee of the loan. Full underwriting approval still needs to happen before you can finalize your mortgage.

For example, if a first-time homebuyer earns $60,000 annually, has a credit score of 720, and no major debts, they may be pre-approved for a $250,000 loan. This number is based on general loan criteria but will need to be confirmed through the underwriting process.

What Is Conditional Approval?

Conditional approval is a step further into the lending process. This type of approval comes after you’ve submitted an application and the lender has done a detailed review of your financials. The key difference is that it isn’t a final loan commitment yet—it’s a preliminary approval, subject to certain conditions being met.

Conditional Approval Process:

-

- Documents Needed: A more in-depth look at your financial situation, including appraisals, title reports, and specific property details.

-

- Outcome: A loan commitment, pending fulfillment of specific conditions (like additional documentation or an approved property appraisal).

-

- Reliability: Conditional approval is stronger than pre-approval, as it indicates that the lender is largely satisfied with the application, but they still need to verify certain factors.

For instance, an investor might be conditionally approved for a $500,000 loan, but the approval could hinge on the appraisal value of a specific property or on providing additional tax returns to verify income.

Key Differences Between Conditional vs Pre-Approval

To gain a clearer understanding of these stages, let’s explore the key differences:

Real-Life Example:

- Pre-Approval: A first-time homebuyer gets pre-approved for $250,000 but may still be rejected if their credit score drops or if the property appraisal falls short.

- Conditional Approval: The same buyer could receive conditional approval for $250,000, but the final approval will depend on the appraised value of the property and the verification of other documents.

How Each Impacts Homebuyers, Investors, and Real Estate Professionals

For Homebuyers:

- Pre-Approval gives you a clear budget and shows sellers you are serious. However, it’s not the final word on your ability to get a loan.

- Conditional Approval is more powerful as it means the lender has already reviewed your financials in depth, making it more likely that your loan will be finalized without surprises.

For Real Estate Investors:

- Pre-Approval helps investors know how much they can spend and can be a great starting point.

- Conditional Approval provides stronger credibility when making offers on investment properties, especially in competitive markets.

For Real Estate Professionals:

- Pre-Approval can guide agents in helping clients find homes within their price range.

- Conditional Approval allows agents to prioritize clients who are closer to finalizing their financing, making transactions smoother and quicker.

How to Make the Most of Pre-Approval and Conditional Approval

Tips for Homebuyers and Investors:

- Start with Pre-Approval: Before you start home shopping, get pre-approved so you know your budget and are ready to make offers quickly.

- Secure Conditional Approval Early: If possible, aim to get conditionally approved before making an offer on a property. This will strengthen your position and make your offer more attractive.

- Stay Prepared: Keep your documents ready—lenders may ask for additional documentation during the conditional approval stage. Being organized speeds up the process.

- Be Realistic About Your Budget: Pre-approval can give you a number, but consider your long-term financial goals to make sure you aren’t stretching your budget too thin.

For Real Estate Professionals:

- Educate Clients: Ensure buyers understand the difference between pre-approval and conditional approval. Help them navigate the process so they can make confident offers.

- Leverage Conditional Approvals: For clients with conditional approval, encourage them to make offers on properties right away. These clients are much closer to getting their financing approved.

Bottom Line

Pre-approval and conditional approval are both important steps in the mortgage process, but they serve different purposes. Pre-approval provides an estimate of how much a lender is willing to lend based on your financial information, but it doesn’t guarantee a loan. Conditional approval, on the other hand, is a stronger commitment, indicating that the lender is mostly satisfied with your financials, but still needs to meet certain conditions before final approval. Homebuyers, investors, and real estate professionals should understand these differences to strengthen their position in the market and ensure a smoother transaction process.